New property is often treated as something to either favour or avoid. That framing misses the point. The more relevant question is whether a newer asset supports the role the property is intended to play within a broader investment strategy.

A property should not be judged on its age alone. It needs to be assessed against cash flow requirements, tax position, borrowing capacity and the intended holding period, rather than considered in isolation. Once those factors are clear, the role of a newer or established property becomes easier to define.

Where new property supports the strategy

New dwellings tend to offer a different financial profile to established stock, particularly when viewed through the lens of long-term holding.

Depreciation and early cash flow

Depreciation is one of the more meaningful variables, and one that is often misunderstood or underutilised.

For investment properties, the Australian Taxation Office (ATO) allows investors to claim deductions for the decline in value of the building (capital works) and certain fixtures and fittings (plant and equipment). For newer properties, these deductions are typically higher in the early years.

Capital works deductions are generally claimed at 2.5% per year over 40 years for residential buildings constructed after 15 September 1987. On a $400,000 construction cost, that can equate to around $10,000 per year in deductions.

Plant and equipment items such as appliances, carpets and air conditioning may also be depreciated over their effective life, which can further increase deductions, particularly in newer properties where these assets are brand new.

In practice, this can improve after-tax cash flow in the early years. This can make a meaningful difference to holding capacity, particularly when interest costs are highest.

Over time, that buffer becomes increasingly important. Stronger early cash flow can make it easier to retain the asset through different market conditions, rather than being forced into decisions driven by short-term pressure. As portfolios grow, this becomes more important as multiple assets increase the impact of cash flow pressure.

Maintenance and cost predictability

Maintenance plays an equally important role, but is often underestimated in planning.

Older properties tend to come with irregular, reactive costs. Repairs are harder to forecast, and without a clear allowance built into the strategy, they can erode returns and place pressure on cash flow at the wrong time.

A newer property, if well built, can reduce that variability in the early years. This is not about avoiding maintenance altogether, but about creating a more predictable expense base within the strategy. This becomes increasingly important when managing multiple properties or holding over longer timeframes.

Tenant demand and rental stability

Tenant demand needs to be considered in practical terms.

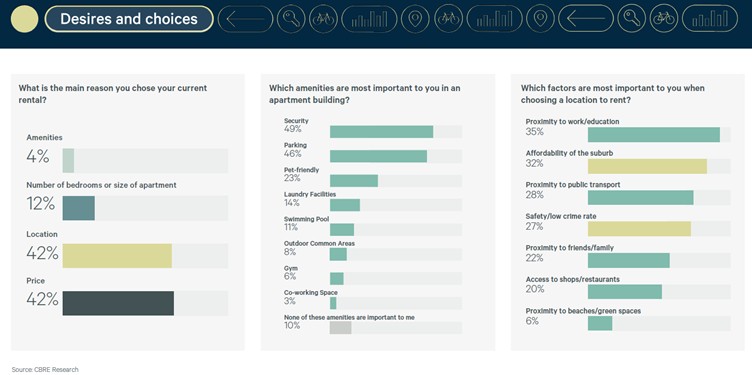

The CBRE/REA Australian Renter Survey 2026 provides a useful reference point for how tenants make decisions. Price and location are equally weighted as the primary drivers, each cited by 42% of respondents, while security, parking and pet-friendly accommodation rank as the most valued apartment amenities.

Tenant demand directly influences vacancy risk, rental stability and long-term performance. A property that aligns with how renters choose homes is more likely to remain occupied and generate consistent income over time.

Newer dwellings can play a role here, but only where they meet these expectations in a meaningful way. Features such as functional layouts, practical inclusions and liveability are often built into newer developments, which can reduce the need for additional capital expenditure to bring a property up to market standard.

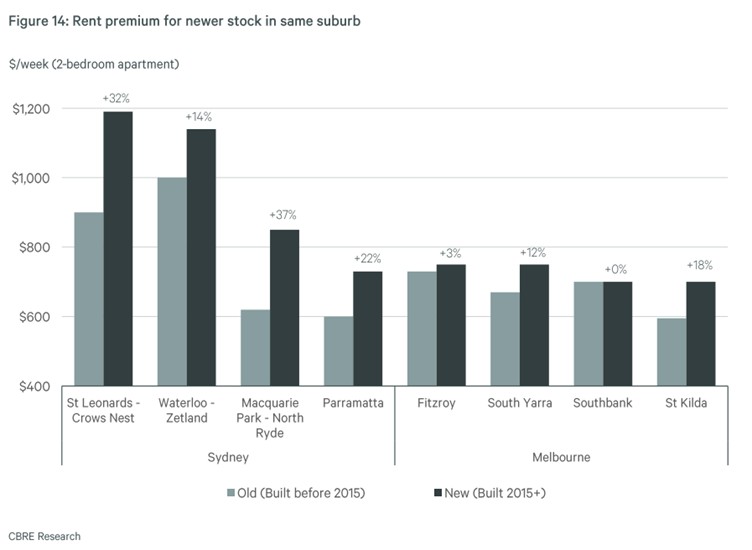

There is also some evidence that this alignment can translate into rental premiums. A separate CBRE analysis of around 3,000 apartments found newer Sydney apartments can achieve rents 20% to 35% higher than older stock, with Melbourne showing a smaller premium.

This is not guaranteed, but it highlights the potential upside where design, amenity and location are aligned.

Understanding the trade-offs

These benefits do not remove the underlying risks.

Location remains the primary driver of performance. A well-presented asset in an area with limited demand or oversupply will struggle regardless of its age.

Developer quality is another key variable. Build quality, design and long-term durability can vary significantly, and assuming all new properties perform the same is a common mistake.

Pricing needs to be assessed carefully. New properties often come with a premium. That premium needs to be justified by long-term demand, not short-term appeal or marketing incentives.

New vs established is the wrong question

The debate between new and established property is often framed as a matter of preference. A more useful approach is to assess how each option contributes to the overall strategy.

A newer property may suit an investor focused on stable cash flow, predictable costs and tax efficiency in the early years. An established property may offer value-add opportunities, stronger land content or access to supply-constrained locations.

The distinction is not which is better in isolation, but which is appropriate given the investor’s full financial position.

A well-structured portfolio is built with clear intention. Each asset should serve a defined purpose, contribute to long-term performance and align with broader financial objectives.

At SAFORE, we approach property as one part of a broader financial strategy. If you are weighing up whether a new property fits within your position, a strategy session can help you assess the role it should play. You can book a time here.